Halla Cast (125490): A Quantum Leap via AI Mobility and Humanoid Robotics

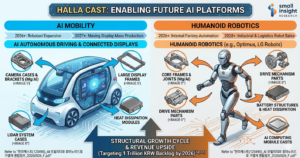

Halla Cast (125490) is rapidly evolving from a traditional automotive parts manufacturer into a cutting-edge lightweight materials platform company. With its advanced technologies in Magnesium (Mg), Aluminum (Al), and Zinc (Zn) precision die-casting, the company is successfully penetrating the core value chains of future industries, including AI autonomous vehicles, connected displays, EV electrification, and humanoid robots.

Here is a deep dive into why Halla Cast is entering a structural growth cycle.

🚀 Key Investment Points

1. Surging Backlog in High-Margin Future Tech

Halla Cast has secured an impressive order backlog. The confirmed mass-production value from 2026 onwards (based on orders won between 2022 and 2025) has surpassed the 1 trillion KRW mark.

- Order Breakdown: Displays (641.9 billion KRW), Autonomous Driving (350.5 billion KRW), Electric Conversion (95.6 billion KRW), Robotics (12.4 billion KRW), and Batteries (11.2 billion KRW).

- Customer Lock-in: These aren’t just simple exterior car parts; they are critical AI electronic structural components involving long-term projects, creating a strong customer lock-in effect. Major domestic clients include LG Electronics, Hyundai Mobis, and Samsung Electro-Mechanics, with end-users spanning global OEMs like Hyundai, Kia, BMW, Mercedes-Benz, Volkswagen, and General Motors.

2. The Global AI Car & Humanoid Momentum

The most significant mid-to-long-term momentum for Halla Cast is its partnership with a global AI automotive company.

- Tier-1 Status: The company was registered as a Tier-1 vendor for this global AI car company in February 2025.

- Humanoid Expansion: In May 2025, Halla Cast secured orders for three key humanoid robot parts (including core frames and driving mechanisms).

- Future Pipeline: Discussions are reportedly underway for supplying about 10 additional components, such as main frames, joint structures, and heat dissipation systems, targeting mass production in the second half of 2026.

AI autonomous driving and humanoid industries require highly integrated semiconductors, which demand superior heat dissipation and lightweighting—areas where Magnesium and Aluminum are essential. Magnesium, in particular, is about 30% lighter than aluminum and boasts excellent EMI shielding and heat dissipation properties.

3. Expansion & Automation Strategy

To meet the explosive demand from the AI mobility and robotics sectors, Halla Cast is aggressively expanding its capacity:

- Plant 1 (Building C): Completed in February 2026, this facility is designed for mass-producing parts for autonomous driving, displays, and robots.

- Plant 2 Expansion: Scheduled for completion in July 2026, this will increase the company’s total production capacity to approximately 150% of its previous level.

- Smart Factory: An automated smart factory system based on MES is being implemented, which is expected to boost production volume by 20-30% once operational.

- Global Footprint: Its production base in Vietnam, established in 2016, serves as a strategic asset for supplying global OEMs seeking to diversify away from China due to geopolitical risks.

4. Passive Fund Inflows

Halla Cast is set to be included in the KOSDAQ 150 index on June 12, 2026, and the S&P Global BMI index in March 2026. This inclusion fulfills the criteria for global institutional investments. The KOSDAQ 150 ETF tracking size is projected to quadruple from 4 trillion KRW in late 2025 to 16 trillion KRW by March 2026, anticipating a strong passive buying effect and improved liquidity.

📊 Financial Outlook & Valuation

- Revenue Growth: Revenue has shown consistent growth from 122 billion KRW in 2023 to 144.4 billion KRW in 2024, reaching 155.8 billion KRW in 2025.

- Profitability Shift: Profitability is expected to level up as the business portfolio shifts from low-margin general auto parts to high-value areas like autonomous driving, displays, and robot frames. Once mass production begins for these complex, high-barrier components, price competition pressure drops, favoring long-term supply profitability.

- Rating: Not Rated (NR). While the upside direction as an advanced lightweight material platform is clear, the “Not Rated” status reflects uncertainties regarding the initial stages of the humanoid market, macro-economic factors slowing EV growth, and raw material price risks. The current PER stands at 165.42 (2025 consolidated estimate).

Disclaimer: This post is a summary of the Small Insight Research report dated May 26, 2026. It does not constitute investment advice. Investors should make decisions based on their own judgment.